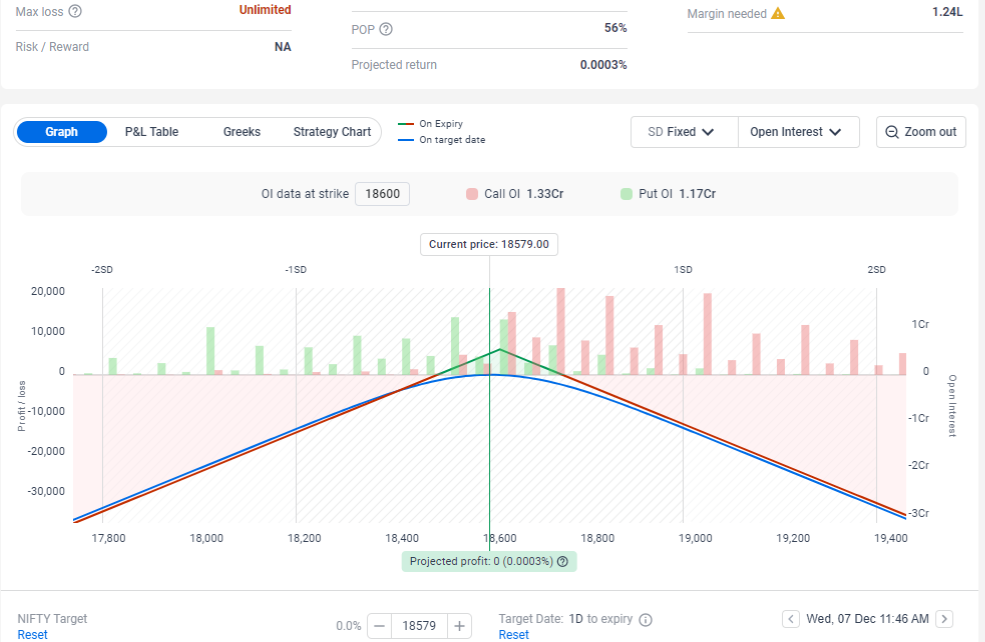

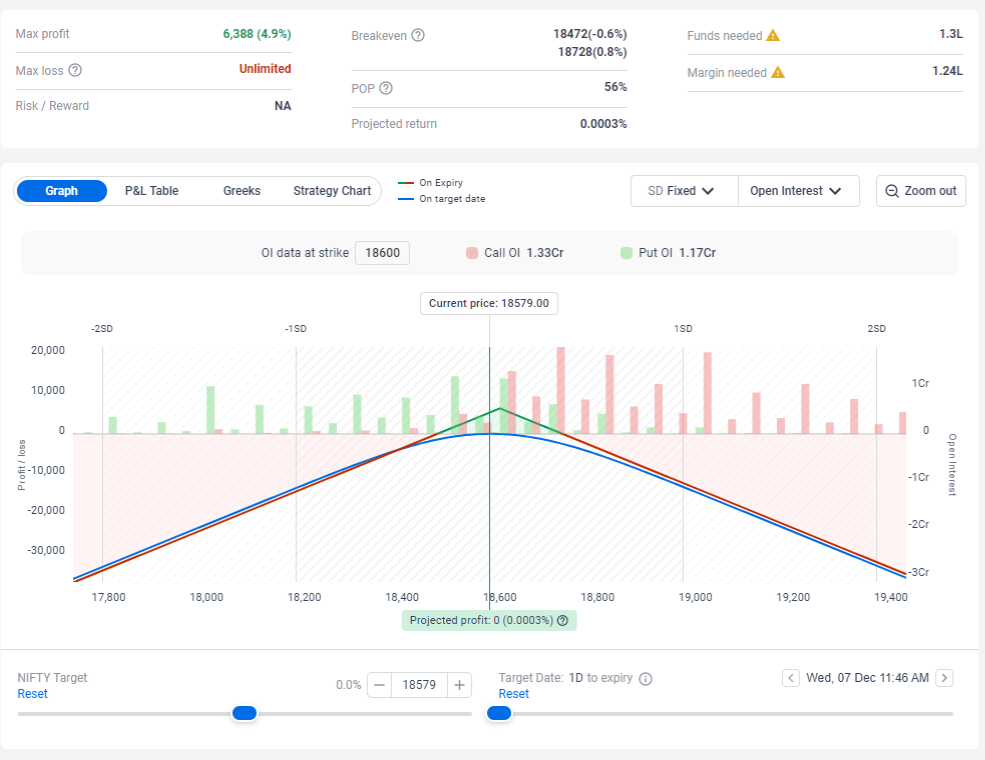

Short Straddle Options Strategy

Theta decay is a concept in options trading that refers to the decrease in the value of an option over time. This is because options have a limited lifespan, and as the expiration date of the option approaches, the likelihood of the option being exercised decreases. As a result, the value of the option will decrease, a phenomenon known as theta decay.

Short Straddle Options Strategy , where a trader sells both a call and a put option with the same strike price and expiration date. This strategy allows the trader to profit from the theta decay of the options, as the trader will collect the premium from the options they have sold. However, the trader will also be at risk of losing money if the price of the underlying asset moves significantly in either direction.

Overall, theta decay is an important concept for options traders to understand, as it can affect the value of their options positions over time. By using strategies that take advantage of theta decay, traders can potentially increase their profits and manage their risks more effectively.

A short straddle is a neutral option trading strategy that involves selling a put option and a call option with the same strike price and expiration date. This strategy is typically used when the trader expects the underlying stock to remain stable and does not expect significant price movements in either direction.

By selling the put and call options, the trader collects the premium from the options, but also assumes the risk of having to buy or sell the underlying stock at the strike price if the options are exercised.

The main risk of a short straddle strategy is that the trader could face significant losses if the underlying stock experiences a sharp price movement in either direction. This is because the trader has sold the put and call options, and therefore has a limited profit potential from the options premiums. If the stock price moves significantly higher or lower than the strike price, the trader may have to buy or sell the underlying stock at a loss.

Also Read : Best Algo Trading Strategy